This is pt.2. Pt.1 covers the raw materials overview.

The first post catalogued what AI hardware is made from. This one tries to answer a more specific question: where in the supply chain does the actual geopolitical leverage sit?

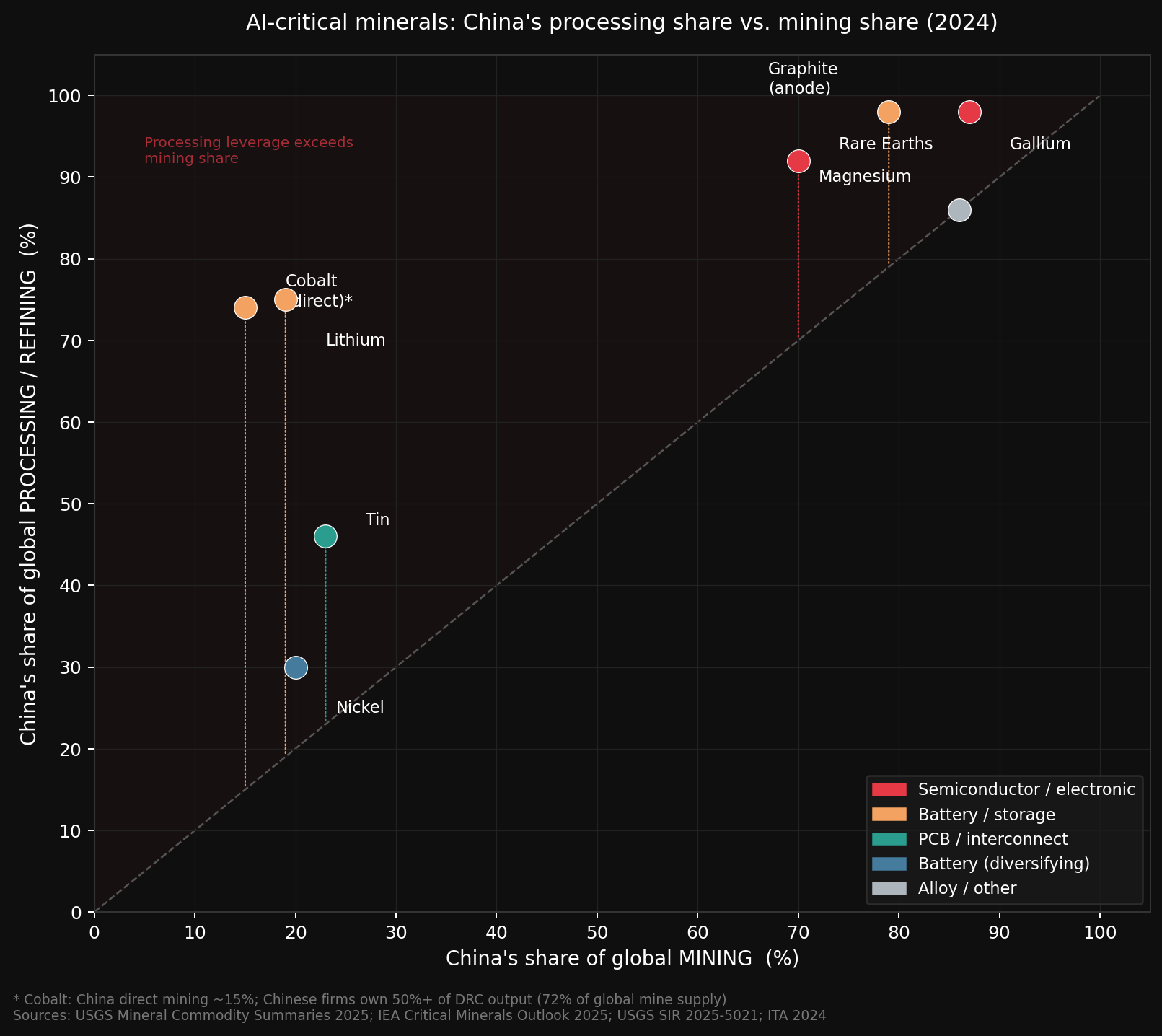

The assumption most people carry is that it sits at extraction. For almost every mineral that matters for AI hardware, China’s share of refining and processing is substantially higher than its share of mining. Often dramatically so.

Cobalt is the clearest example. The DRC mines 72% of global cobalt. China mines 15% directly and refines 74%. The DRC extracts ore it has almost no downstream capacity to transform. China imports concentrate and returns finished industrial inputs. The leverage doesn’t sit at the mine. It sits at the refinery.

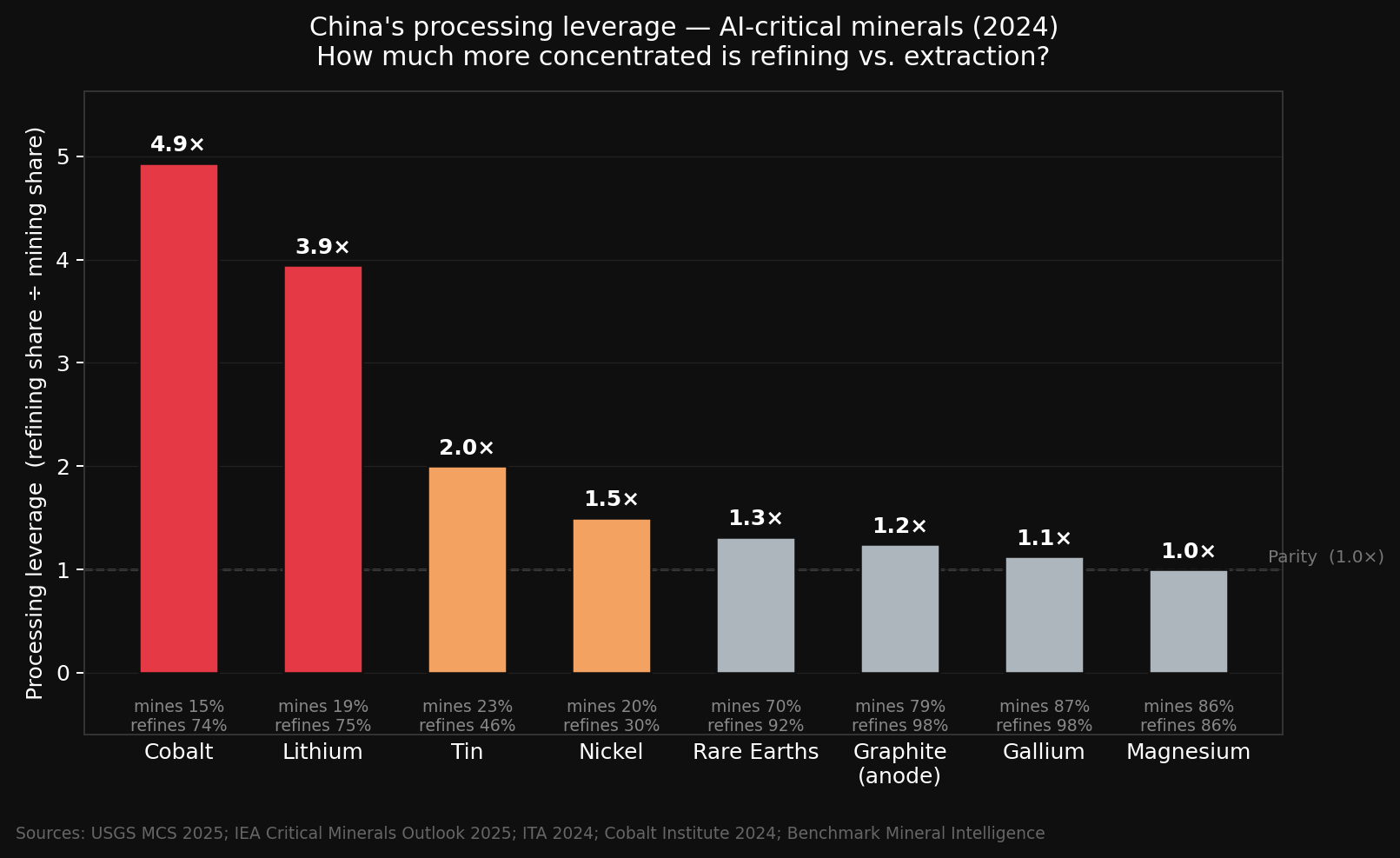

I went through eight minerals directly relevant to AI hardware and computed a ratio: refining share divided by mining share. Call it processing leverage.

| Mineral | China mines | China refines | Leverage |

|---|---|---|---|

| Cobalt | 15% | 74% | 4.9x |

| Lithium | 19% | 75% | 3.9x |

| Tin | 23% | 46% | 2.0x |

| Nickel | 20% | 30% | 1.5x |

| Rare Earths | 70% | 92% | 1.3x |

| Graphite (anode) | 79% | 98% | 1.2x |

| Gallium | 87% | 98% | 1.1x |

| Magnesium | 86% | 86% | 1.0x |

Sources: USGS MCS 2025, IEA Critical Minerals Outlook 2025, ITA 2024, Cobalt Institute 2024, Benchmark Mineral Intelligence

Cobalt and lithium are the outliers. Both above 3x, meaning China refines roughly four times what it mines. That’s not geology. It reflects decades of deliberate industrial policy: building the downstream capacity to convert raw ore into battery-grade chemical inputs, while the rest of the world built relatively little.

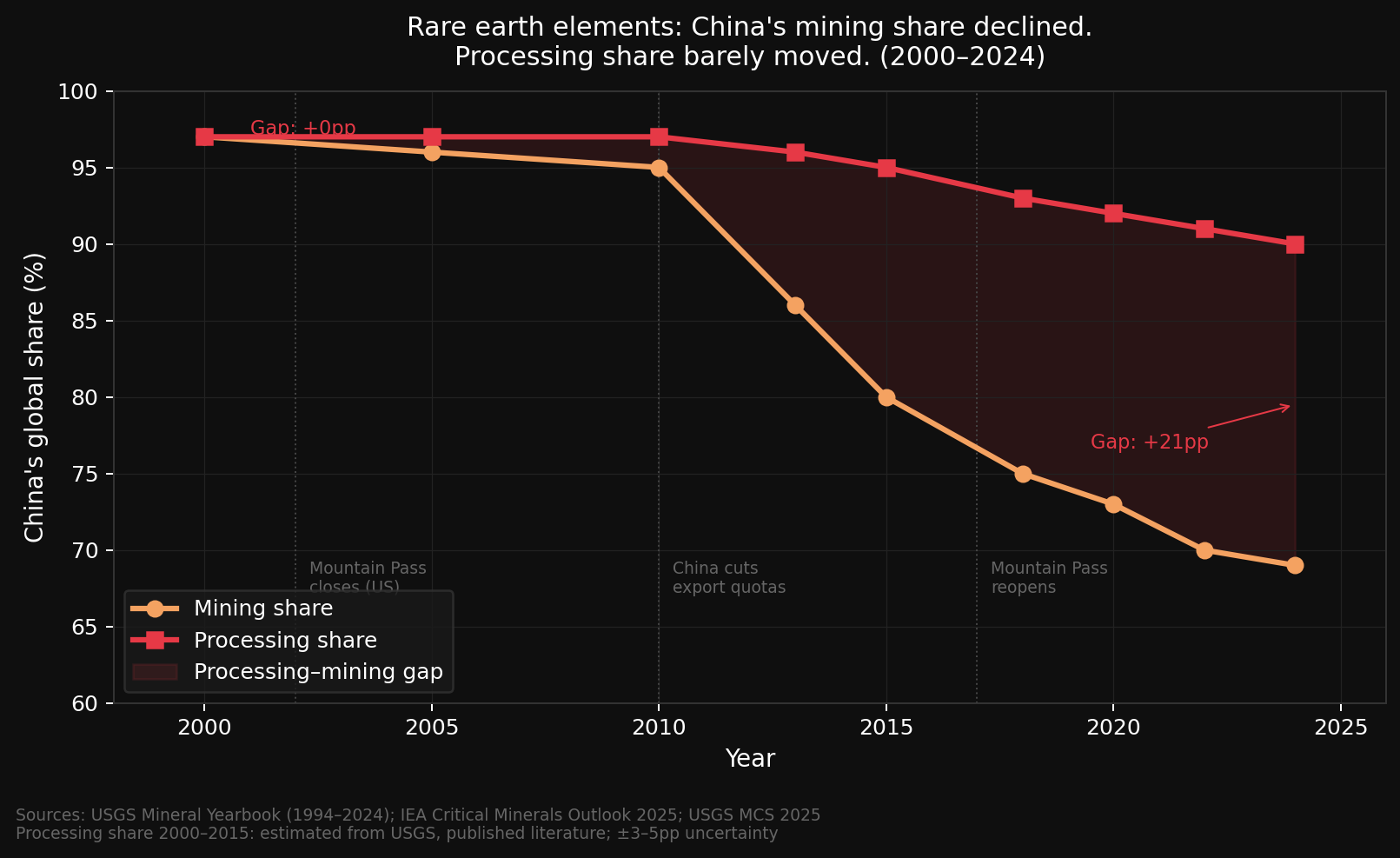

In 2000, China’s mining share and processing share for rare earths were both around 97%, identical. Over twenty-five years, they diverged. Extraction diversified: Australia’s Mount Weld came online, Myanmar scaled exports, Mountain Pass in California reopened. By 2024, China’s mining share had fallen to 69%. The processing share moved to 90%. The gap went from zero to 21 percentage points in a single generation. The world diversified where minerals are extracted, but not where they are industrially transformed. Building a mine and building a refinery are different problems. One requires capital and a viable deposit. The other requires years of process chemistry development, purpose-built industrial infrastructure, and a workforce with skills that take decades to accumulate at scale. The West built the mines. The refineries didn’t follow.

The cluster arithmetic makes this concrete.

A 100,000-GPU H100 cluster is a 166 MW facility. Based on NVIDIA DGX H100 specifications and hyperscale copper intensity data: 12,500 servers at roughly 10 kW each, plus overhead. At the copper intensity typical of hyperscale AI data centers (27 to 33 tonnes per megawatt), that facility embeds between 4,500 and 5,500 tonnes of copper. The UPS backup system, twelve minutes at full load, requires around 204 tonnes of lithium-ion batteries, containing 4 tonnes of lithium and 102 tonnes of graphite. Close to all of that graphite will have passed through Chinese processing.

GPUs and fabs get the attention. Electricity has become a known constraint.

Processing leverage describes a specific exposure: not where minerals are found in the ground, but where they’re converted into something industrial systems can actually use. Reserves are geology. Processing capacity is policy.

There’s no shortage of lithium in the ground. There’s a shortage of plants that can convert spodumene concentrate into battery-grade lithium hydroxide outside of China. Building those takes capital, permitting, a decade of lead time, and process chemistry expertise that doesn’t exist at scale in the West yet.

Frontier AI is a physical industrial problem. The electricity constraint is now visible. The refining constraint, mostly, isn’t.

Data: USGS MCS 2025 (Jan 2025), USGS SIR 2025-5021, IEA Critical Minerals Outlook 2025 (May 21 2025), ITA 2024, Cobalt Institute 2024, Benchmark Mineral Intelligence. Cluster arithmetic from NVIDIA DGX H100 datasheet and copper.org/SDxCentral. Post dated to May 21 2025 — earliest date all sources were available.