AI is not purely digital infrastructure. It is an industrial system.

Last year, went down the rabbit hole on earth materials and how they fit into the theme of supply chain demand, particularly with the growth of compute required AI. Defense contracts heavily depend on lithium, especially for electronic components and warfare applications. Currently, the US mainly rely on outsourcing lithium from countries such as China and Australia.

The interesting realisation is that the bottlenecks increasingly look less like traditional software constraints and more like industrial coordination problems.

A large AI cluster is a physical object. It requires: high electrical load, specialised cooling systems, high-purity quartz, advanced packaging, copper-heavy interconnects, tin solder (?), lithium-backed energy systems, and, globally distributed mineral processing chains.

Which makes the geopolitical structure unusually asymmetric.

Core Components of AI Compute

At the heart of systems; powerful computing units that require a variety of minerals and materials:

- Central Processing Units (CPUs) and Graphics Processing Units (GPUs):

Require silicon, copper, and gold

Key players:

NVIDIA: Dominates the AI GPU market

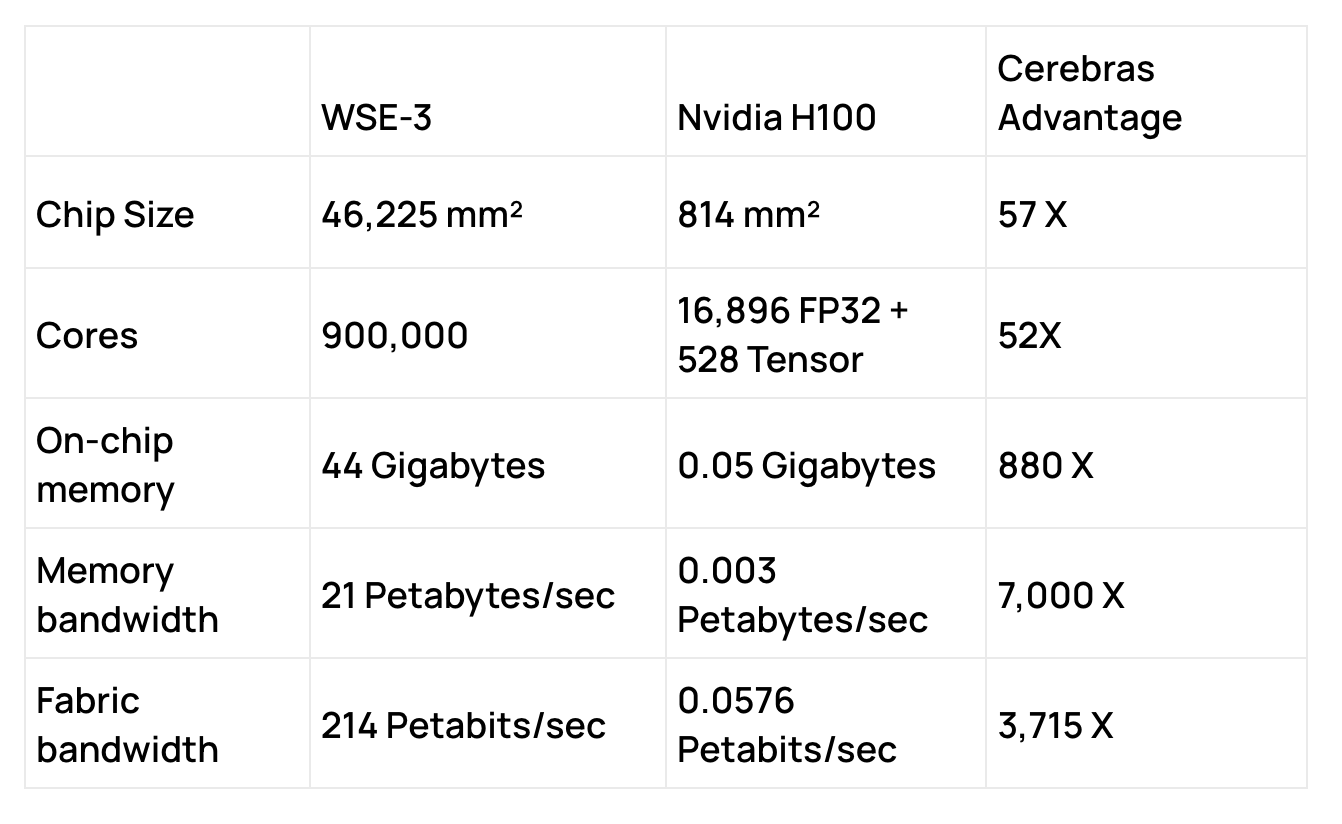

Cerebras Systems: Developed the world’s largest AI chip, the WSE-3

Graphcore: Creating Intelligence Processing Units (IPUs) for AI workloads

High-performance CPUs

Large amounts of memory and storage

High-speed interconnects

Power supply and cooling systems

Raw materials required:

Central Processing Units (CPUs) and Graphics Processing Units (GPUs): The brains of computing, requiring silicon, copper, and gold.

NVIDIA: Dominates the AI GPU

Cerebras Systems: Developed the world’s largest AI chip, the WSE-3

Graphcore: Creating Intelligence Processing Units (IPUs) for AI workloads

Semiconductors:

- Essential for all electronic devices, relying heavily on silicon, germanium, and gallium arsenide.

Memory Storage Devices:

Utilising materials like cobalt, nickel, and rare earth elements.

Western Digital offers high-capacity storage solutions for AI data centers.

Printed Circuit Boards (PCBs):

Incorporating tin, copper, and gold for electrical connections.

TTM Technologies: Major PCB manufacturer

Flex: Provides PCB assembly services for AI hardware

Material Composition in AI Hardware

Silicon: ~25% of a semiconductor chip by weight

Copper: ~12% of electronic devices

Gold: <0.1% by weight, crucial for reliable PCB connections

Tin: ~3% of PCB weight, used in soldering

Estimated TAM for AI Hardware by 2025:

AI Chips and Processors: $91 billion (Gartner)

Lithium-Ion Batteries: Over $100 billion (Bloomberg NEF)

Lithium:

Lithium is indispensable for lithium-ion batteries, which power:

Electric Vehicles (EVs): Each EV battery contains about 8 kg (17.6 lbs) of lithium.

Consumer Electronics: Smartphones contain around 0.8 grams of lithium.

Energy Storage Systems: Utility-scale batteries can contain thousands of kilograms of lithium.

Global Lithium Consumption by Sector (2020):

Batteries: 65%

Ceramics and Glass: 18%

Lubricating Greases: 5%

Continuous Casting Mold Flux Powders: 3%

Other Uses: 9%

Currently, the majority of lithium comes from:

Australia: The largest producer, mainly through hard-rock mining. 52% of global production

Chile and Argentina: Rich in lithium brine deposits. 22% and 8% of global production

China: Not only a producer but also a major processor of lithium. 13% of global production

Lithium Americas Corp: Developing lithium projects in the U.S. and Argentina

Piedmont Lithium: Focused on developing lithium resources in North Carolina

Quartz: The Foundation of Semiconductors

High-purity quartz is essential for:

Semiconductor Manufacturing: Quartz crucibles are used to grow silicon ingots.

Optical Fibers: Making up the core of fiber-optic cables.

Usage Breakdown:

Semiconductors: Approximately 60% of high-purity quartz consumption.

Optical Applications: 25%

Solar Panels: 15%

Global Sources:

Quartz mining is more geographically diverse but still concentrated in specific regions with high-purity deposits.

United States: Significant producer of high-purity quartz.

Norway and Russia: Other notable producers.

Tin: The Glue

Tin is primarily used in:

- Solder: An alloy (often with lead or silver) used to join metal components in PCBs.

Tin Usage in Electronics:

Solder: Accounts for 50% of global tin consumption.

Tinplate: 17%

Chemicals: 13%

Brass and Bronze: 5%

Others: 15%

A typical PCB contains about 2-3% tin by weight.

Global Sources:

China: 31% of global production.

Indonesia: 27%

Myanmar: 17%

Peru and Bolivia: Combined 11%

See AFM Resources Deep Dive for more.

China’s Dominance

Rare Earth Elements: China controls about 80% of global supply.

Production: China accounts for approximately 60% of global rare earth element production

Processing: 85% of rare earth processing occurs in China

Source: Ezrati M. Article, 2023

Processing Capabilities: Even when mined elsewhere, many minerals are processed in China.

Potential Leverage: Export controls on minerals like lithium and tin could impact global tech industries.

Impact on the U.S. Tech Sector

Dependency: The U.S. imports over 50% of its lithium and over 75% of its tin.

Export Restrictions: Recent bans on REE exports to the United States in retaliation for chip sales restrictions. The Department of Defense has labeled China as the top strategic threat, partly due to this mineral dependency

Historical Precedent: Previous export bans on Japan during territorial disputes

Strategic Vulnerability: Reliance on imports from geopolitically unstable regions poses risks to national security and technological leadership.

Critical Minerals Strategy:

Aims to secure reliable supplies of minerals essential for national security and economic prosperity.

Executive Order 13817: Issued in 2017 to ensure secure and reliable supplies of critical minerals.

Financial Incentives: Tax credits and grants for companies investing in domestic mineral extraction and processing.

Public-Private Partnerships: Collaborations to develop sustainable mining technologies.

Western North Carolina: A Domestic Opportunity

Lithium Reserves:

Kings Mountain and Gaston County: Estimated to contain over 2 million metric tons of lithium spodumene reserves.

Potential Contribution: Could supply up to 10% of global lithium demand.

Quartz Deposits:

- Asheville Region: Home to high-purity quartz, suitable for semiconductor manufacturing.

These domestic reserves present an opportunity for the U.S. to reduce its reliance on imports. According to the U.S. Geological Survey, tapping into these resources could bolster the national supply chain for critical minerals.

Technological Hurdles

Extraction Technologies: Developing efficient and eco-friendly mining methods.

Processing Capabilities: Building facilities to refine raw materials domestically.

2. Investment Areas

2.1 Sustainable Mining Technologies

Opportunity: Develop and deploy technologies that minimize environmental impact while increasing extraction efficiency.

2.2 Domestic Processing and Refining

Opportunity: Processing facilities in the U.S. to reduce dependency on foreign entities.

2.3 Recycling and Resource Recovery

Opportunity: Invest in technologies that recycle end-of-life batteries and electronics to reclaim critical minerals.

2.4 Alternative Materials and Technologies

Opportunity: Research and develop substitutes for critical minerals or entirely new technologies that reduce reliance on scarce resources.

Solid-State Batteries:

- Lithium Alternatives: Exploring sodium-ion or magnesium-based batteries.

3.1 Existing Players

Large Mining Corporations: Companies like Albemarle and SQM dominate lithium mining but are less agile in adopting new technologies.

International Processing Firms: Chinese firms lead in processing but face geopolitical scrutiny.

3.2 Barriers to Entry

Capital Intensity: High initial investment for mining and processing facilities.

Regulatory Compliance: Navigating environmental laws and obtaining necessary permits.

Technical Expertise: Requires multidisciplinary teams with expertise in geology, engineering, and environmental science.

Emerging Players

MP Materials (USA):

Operates the Mountain Pass mine in California, providing 15% of global rare earth supply

Developing a complete domestic supply chain, including a magnetics manufacturing facility in Fort Worth

USA Rare Earth:

- Developing the Round Top Mountain deposit in Texas, aiming to produce 15 of the 17 rare earth elements.

Rare Element Resources (USA):

- Advancing the Bear Lodge Project in Wyoming, one of the highest-grade rare earth deposits in North America.

Piedmont Lithium:

Developing an integrated lithium business in Gaston County, North Carolina.

Aims to be a strategic domestic supplier of battery-grade lithium hydroxide and other lithium products

Albemarle Corporation:

Expanding its lithium operations in Kings Mountain, North Carolina.

Investing in both mining and processing capabilities to create a vertically integrated lithium supply chain

Emerging technologies

Direct Lithium Extraction (DLE) Technologies:

- Companies like Eramet are pioneering DLE methods that could revolutionise lithium extraction from brines

Unconventional Lithium Sources:

Geothermal and oilfield brines are emerging as potential lithium sources, with grades of 100 to 200 ppm

Companies like Renault Group, Stellantis, and General Motors are partnering with geothermal lithium projects in North America

Adsorption DLE:

- Companies like Sunresin are developing adsorption-based DLE technologies for more efficient lithium extraction from brines

Ion Exchange and Membrane Separation:

- Emerging DLE technologies using ion exchange and membrane separation processes show promise for increasing lithium recovery rates and reducing environmental impact

Solid-State Batteries:

Research into solid-state batteries could reduce reliance on liquid electrolytes, potentially decreasing the demand for certain critical minerals.

Exploration of sodium-ion and magnesium-based batteries as potential alternatives to lithium-ion batteries, diversifying the battery material landscape.